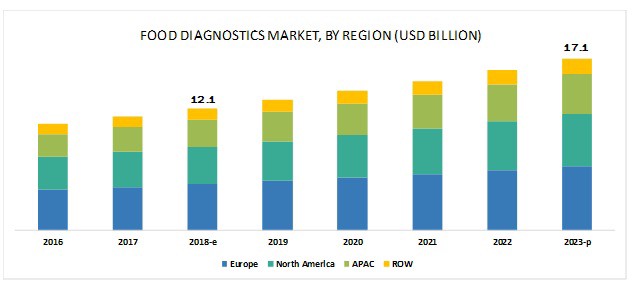

The food diagnostics market is projected to grow from USD 12.1 billion in 2018 to USD 17.1 billion by 2023, at a CAGR of 7.1% during the forecast period. This is attributed to the increasing incidence of foodborne illness, globalization in food trade, and the rise in demand for efficient, reliable, and real-time food testing.

By type, the hybridization-based segment is projected to be the largest contributor in the food diagnostics market during the forecast period.

PCR and microarray systems have become a powerful tool for food analysis due to their high analytical precision, user-friendly procedures, and accurate output in food diagnosis. Additionally, the hybridization-based systems are the most preferred diagnostics systems for the detection and quantification of foodborne pathogens. These systems are also used to identify the mutations in food pathogens, which are responsible for chronic infections. Due to such advantages of the hybridization-based systems in the detection of food contaminants, the food diagnostics market is projected to drive the growth of this market.

The meat, poultry, and seafood segment is projected to account for a larger market share during the forecast period.

Among foods tested, the market is estimated to be dominated by the meat, poultry, and seafood segment in 2018. The contamination of meat & poultry products is often observed during processing, packaging, and storing. The Food Safety and Inspection Service (FSIS) has framed regulations to control the contamination of meat & poultry products in slaughterhouses and processing plants, based on the HACCP food safety control system. A major factor that drives the growth of the seafood testing products market is the high demand for seafood products such as crustaceans, shrimp, crabs, lobsters, tuna, marlin, and swordfish, due to their nutritional values such as the presence of omega fatty acids and other essential nutrients.

Europe is projected to account for the largest market share during the forecast period.

The European market accounted for the largest share in the food diagnostics market. European countries have recorded many issues related to food safety over the past few years. As a result, stringent policies were introduced to implement complete food safety solutions for the consumers. In Europe, food safety policies have been emphasized by efforts from Control Laboratories (CLs), National Reference Laboratories (NRLs), and EU Reference Laboratories (EURLs). These authorities play an important role in maintaining food standards and protecting consumer health by ensuring the quality of the food supply chain. This will subsequently, propel the growth of the food diagnostics market in Europe.

Key Market Players

The major vendors in the global food diagnostics market are 3M Company (US), Merck KGaA (Germany), Thermo Fisher Scientific Inc. (US), FOSS (Denmark), and Agilent Technologies Inc. (US). Some of the other players that hold a significant share in the market include bioMérieux SA (France), Danaher Corporation (US), Bio-Rad Laboratories, Inc. (US), Neogen Corporation (US), Biorex Food Diagnostics (UK), Randox Food Diagnostics (UK), Hygiena, LLC (US), Qiagen (Germany), EnviroLogix Inc. (US), and GEN-IAL GmBH (Denmark). These players have broad industry coverage and strong operational and financial strength; they have grown organically and inorganically in the recent past. The industry players, such as Merck KGaA (US) acquired BioControl Systems, Inc. (US), a global provider of food safety testing systems. The acquisition helped the company to strengthen its life science segment by allowing it to reinforce its food safety market with a complete workflow solution for food pathogen testing. Through this acquisition, the company expands in food diagnostics product line, thereby strengthening its leading position for food diagnostics systems and consumables in globally, in 2017.